Property management is the operation, control, maintenance, and oversight of real estate and physical property. This can include residential, commercial, industrial, public capital, and land real estate.[1] Management indicates the need for real estate to be cared for and monitored, with accountability for and attention to its useful life and condition.[2][3] This is much akin to the role of management in any business.

Property management is the administration of personal property, equipment, tooling, and physical capital assets acquired and used to build, repair, and maintain end-item deliverables. Property management involves the processes, systems, and workforce required to manage the life cycle of all acquired property as defined above, including acquisition, control, accountability, responsibility, maintenance, utilization, and disposition.

An owner of a single-family home, condominium, or multi-family building may engage the services of a professional property management company. The company will then advertise the rental property, handle tenant inquiries, screen applicants, select suitable candidates, draw up a lease agreement, conduct a move-in inspection, move the tenant(s) into the property and collect rental income. The company will then coordinate any maintenance issues, supply the owner(s) with financial statements and any relevant information regarding the property, etc.

Roles and Responsibilities

Property management involves a wide range of tasks and responsibilities carried out by property managers, management companies, or individual landlords. Property managers serve as the operational backbone of real estate ownership, balancing the financial interests of the owner with the comfort and satisfaction of tenants while maintaining the property’s long-term value.[2][3]

The specific roles depend on the type of property[1]—residential, commercial, or industrial—but generally include:

Tenant Relations

Property managers act as intermediaries between property owners and tenants. They handle tenant inquiries, process applications, conduct screenings, negotiate lease agreements, and coordinate move-in and move-out procedures. In most settings, property management companies also operate the mailroom of the buildings in which they lease to tenants or manage on behalf of the landlord client; Mailroom Operations is a component of property management.

Rent Collection and Financial Management

Managers are responsible for collecting rent, enforcing payment terms, issuing late notices, and managing security deposits. Many also prepare financial statements, budgets, and reports for property owners, ensuring compliance with local and national regulations.

Maintenance and Repairs

A key role of property management is the maintenance of the property. This includes scheduling regular inspections, coordinating repairs, overseeing contractors, and ensuring that the property meets safety and habitability standards.[4]

Facilities management (or facility management) is a professional discipline within property management, focused on coordinating the use of space, infrastructure, people, and organizational resources to ensure that physical assets and environments are managed effectively to meet the needs of their users.[5][4]

Property managers must ensure that the property adheres to housing laws, landlord-tenant regulations, fair housing rules, and zoning ordinances. They may also handle evictions and represent owners in legal proceedings related to tenancy issues.

Marketing and Leasing

In residential and commercial contexts, managers are often responsible for advertising vacancies, setting rental rates based on market conditions, and maintaining high occupancy levels through effective marketing strategies.

Administrative Duties

Administrative responsibilities may include record-keeping, contract management, insurance coordination, and maintaining communication with property owners and vendors.

Property Management Business Pricing Models

Percentage of rent

The percentage of rent model is the most common property management model, typically used by companies managing multi-unit residential buildings and single-family homes. In this arrangement, the property owner enters into a management agreement granting the company the authority to lease the house or property to new tenants and collect rent on the owner’s behalf. Property owners are generally not directly involved with tenants and may not even know their identities. The management company usually retains between 8% and 12% of the rental income as a management fee, remitting the remainder to the property owner.[6][7][8]

Flat-fee / Fixed-fee

A fixed-fee property management model, also known as a flat-fee model, is an alternative to the traditional percentage-based structure. In this arrangement, the property management company charges a predetermined monthly or annual fee for its services, regardless of the property’s rental income. This model is often preferred by property owners seeking predictable management costs, especially for higher-rent properties where a percentage-based fee could result in higher expenses.

Under a fixed-fee agreement, the scope of services—such as tenant placement, rent collection, maintenance coordination, and property inspections—is typically defined in advance. Some companies offer tiered or customizable service packages to accommodate different owner needs. The fixed-fee model has gained popularity in recent years due to its transparency, cost stability, and appeal to investors managing multiple rental units.

The flat-fee model is also popular among vacation property owners who do not wish to rent out their properties but want a management company to oversee maintenance, inspections, and general upkeep.[9]

Hybrid Pricing Model

A growing trend in property management, is the hybrid pricing model, which combines elements of both percentage-based and fixed-fee structures. Under this approach, property management companies charge a reduced percentage of the monthly rent along with a flat administrative fee. This model aims to balance affordability and service flexibility, providing property owners with predictable costs while ensuring management companies maintain sustainable revenue for operational expenses.[10]

Guaranteed rent

This model is also used in the residential space, but mostly for small units in high-demand locations. Here, the company signs a rental agreement with the owner and pays them a fixed rent. As per the agreement, the company is given the right to sublet the property for a higher rent. The company’s income is the difference between the two rents. As is evident, in this case, the company minimizes the rent paid to the owner, which is usually lower than market rates.[11]

Revenue share / Percentage Lease

A percentage lease is a type of commercial lease commonly used in retail environments, particularly in shopping centers and other high-traffic locations. Under this arrangement, the tenant pays a fixed base rent in addition to a percentage of their gross sales that exceed a specified amount, known as the breakpoint. This structure aligns the interests of the landlord and tenant by allowing rent to fluctuate based on the tenant’s sales performance.[12]

Software & Property Technology Solutions

The property management services market has increasingly emphasized technological innovation, largely driven by the adoption of software such as property management systems, hotel operating systems (HOS), and property technology (PropTech) solutions. The global property management software market was valued at approximately USD 5.51 billion in 2023 and is expected to grow to around USD 9.68 billion by 2030.[13]

Many property management firms now utilize artificial intelligence (AI), Internet of Things (IoT)–enabled maintenance systems, mobile applications, and cloud-based platforms to improve operational efficiency and tenant engagement. These technologies facilitate functions such as predictive maintenance, automated rent collection, digital leasing processes, and data analytics for real-time decision-making. As tenant expectations continue to evolve, PropTech has become an integral component of contemporary property management practices.[14][15]

Property Management Licensing

Licensing requirements for property managers vary widely depending on the jurisdiction and type of property but generally aim to ensure professional standards, consumer protection, and ethical business practices within the real estate industry. As a result, Property management is a regulated profession in many countries with licensing requirements designed to protect property owners and tenants alike. The specific requirements vary by country, region, state, etc but in many cases, property managers must hold a real estate broker’s license or a specialized property management license to legally manage rental properties on behalf of others.[16]

To obtain a license, applicants are typically required to complete pre-licensing education, pass a state examination, and undergo a background check. Once licensed, property managers must follow state and/or local laws that govern leasing practices, trust accounting, fair housing compliance, and tenant-landlord relations.

In some places, unlicensed individuals may manage properties they personally own, but cannot legally collect rent, negotiate leases, or represent other property owners without proper licensure. Some places offer exceptions or separate licensing paths for managing community associations, vacation rentals, or commercial properties.

Even in areas without strict licensing laws, many professional property managers voluntarily pursue certification through national organizations such as the Institute of Real Estate Management (IREM) or the National Association of Residential Property Managers (NARPM). These credentials help demonstrate knowledge, professionalism, and a commitment to ethical standards in the industry.

Rent Control Act in the Philippines

Republic Act 9653[1], better known as the Rent Control Act of 2009, is the law that protects housing tenants (especially in the lower-income class) against unreasonable rent increases. It also provides the eviction rules that both landlords and tenants must observe.

This rental law in the Philippines covers housing units with a monthly rent of up to PHP 10,000 in Metro Manila and other highly urbanized cities nationwide.

Particularly, the following rental properties are covered by the Rent Control Act:

Apartments

Boarding houses, bedspaces, dormitories, and rooms for rent

Houses and/or land

Landlords and renters who violate any provision of the rental law face penalties—a fine of PHP 25,000 to PHP 50,000, imprisonment of one month and one day to six months, or both.

Civil Code of the Philippines

The Civil Code[2] has lease provisions that cover rentals above PHP 10,000 and those not covered by the Rent Control Act of 2009, including commercial spaces and rent-to-own units.

The lease provisions in the Civil Code are rather lengthy and too technical for common people to understand. If you’re covered by this rental law in the Philippines and you think your landlord has violated your tenant rights, it’s best to consult a lawyer who specializes in this field.

What are the Rights of a Tenant in the Philippines?

Tenants are entitled to protection as mandated by rental laws in the Philippines. Based on data from the Philippine Statistical Research and Training Institute[3], the majority or 97% of renters in the country are paying monthly rent at PHP 10,000 and below. Thus, in this article, we’ll focus on the tenant rights provisions under the Rent Control Act.

Here are the basic rights you should know if you’re renting a home.

1. Limit on Rent Increases

Landlords cannot increase the rent by more than what the law allows. The Housing and Urban Development Coordinating Council (HUDCC), a government agency that regulates residential leases in the Philippines, has set the rental increase limits[4] based on the Rent Control Act.

Until how much can landlords increase their rent?

Monthly Rent

Maximum Rent Increase

PHP 4,999 and below

2% (only once per year)

PHP 5,000 to PHP 8,999

7% (as long as the unit is occupied by the same tenant)

PHP 9,000 to PHP 10,000

11% (as long as the unit is occupied by the same tenant)

Before you sign a lease agreement, check if it has any provision on rent increase. If it does, it should be within the legal limit.

Also, the Rent Control Act allows landlords to increase rents only once a year for bedspaces, boarding houses, dorms, and rooms leased to students. In this case, no rent increase can be charged twice or more per year even if a new tenant moves into the unit within the same year.

2. No Charging of Excessive Deposit and Advance Rent

Under the Rent Control Act, landlords can only collect not more than two-month deposit and not more than one-month advance rent.

The rental law also requires them to keep the deposit payment in a bank account under the landlord’s name throughout the duration of the lease agreement. When the contract expires, the deposit and the interest it earned, plus any remaining balance from the advance rent, should be returned to the tenant.

However, landlords can use the deposit and advance rent to compensate for losses they incur when tenants fail to pay the rent, settle utility bills, and/or causes damage to any part of the property.

3. No Eviction Without Legal Ground

If your landlord tells you to vacate the house, ask for the specific reason for the eviction. You cannot be evicted for unjust reasons.

When Can a Tenant be Evicted in the Philippines?

The decision to evict a tenant must be based on grounds specified by the rental law in the Philippines. The Rent Control Act allows eviction only for any of the following reasons:

Subleasing – The tenant rents out a portion or all of the unit to another person without the property owner’s written consent.

Overdue rental payments – The tenant has not paid the rent for three months or more.

Owner’s legitimate need to use the property – The landlord or his/her family needs to occupy the unit. In such a case, the tenant can be evicted only after the lease contract expires. The renter should also be given a formal notice to vacate three months in advance.

Necessary house repairs – The landlord has to do necessary repairs on the leased unit to make it safe and suitable to live in. When the repair is finished, the evicted tenant should be the priority in leasing the unit.

Lease contract expiration – The landlord has the option not to renew the rental agreement once it expires. This usually happens when the landlord wants to get rid of unruly or delinquent tenants.

When is Eviction Illegal?

Renters in the Philippines cannot be asked to leave the leased property for any of the following reasons:

1. Sale or mortgage of the property

Under the Rent Control Act, if the landlord has sold or mortgaged the leased unit to a third party, the landlord or the new owner cannot evict the tenant.

2. If you’re a COVID-19 patient or frontliner

If you’re renting in a city with an anti-COVID-19 discrimination ordinance (such as Makati, Manila, Muntinlupa, Pasig, and Quezon City), you shouldn’t be forced to leave your rented unit or be denied of leasing if you’re suspected or infected with COVID-19 or any infectious disease. The same goes for healthcare and emergency workers.

3. Failure to pay rent and other reasons during the quarantine period and grace period

Property owners cannot evict tenants in ECQ, MECQ, and GCQ areas from the start of the quarantine until the end of the mandatory 30-day grace period (which starts from the last due date of rent or from the lifting of the quarantine, whichever is longer).

This rule, which is based on a Department of Trade and Industry (DTI) memorandum circular[5] under the Bayanihan to Heal as One Act, applies to residential tenants and commercial tenants in the MSME (micro, small, and medium enterprise) industry that were banned from operating during the ECQ.

Under the DTI memo, no eviction is allowed even for tenants who fail to settle their rent during the community quarantine. Landlords who refuse to comply with the grace period could be fined at least PHP 10,000, jailed for at least two months, or both.

All unpaid rents during the quarantine period can be settled in six monthly installments—without any penalties, interests, fees, and other charges—after the end of the grace period. According to the DTI, tenants who opt to do that should give their landlord a promissory note or any letter stating their intention to pay the overdue rents in installments.

What Should I Do If My Tenant Rights are Violated?

Rental laws are not clear about what you can do in case your rights as a renter are violated. You can first try to negotiate with your landlord for a settlement. If you don’t reach an agreement, seek the assistance of your barangay chairman or lupon[6], which has the authority to protect landlord and tenant rights.

If your landlord evicts you during the quarantine period, it’s a clear violation of the DTI guidelines on residential and commercial rents[7]. You can file a complaint with the DTI through email or in person. The DTI will then issue a notice of violation to the landlord and require a written reply. Once the violation is confirmed, an appropriate criminal case will be filed with the Department of Justice against the erring landlord.

Final Thoughts

Especially during a crisis, the law gives special consideration to renters struggling to settle their rent. Knowing your tenant rights under the rental laws in the Philippines certainly helps you avoid unfair and stressful situations like illegal eviction.

A condominium offers individuals ownership of their residential unit while providing communal sharing of facilities and maintenance through association agreements.

What Is a Condominium?

A condominium is an individually owned unit within a larger residential complex composed of similar units.

A condo owner typically has shared ownership of community property, such as floors and stairwells, which is managed by the condominium association.

Condos involve ownership, as opposed to rental, like in apartments. Another difference is the monthly fees that condo owners usually pay to a condominium association for property upkeep and common area maintenance.

A condo association or management is usually made up of a board of unit owners who oversee daily operation of the complex, such as lawn maintenance, snow removal, and building updates.

Understanding Condominium Ownership and Management

Condo owners actually own the “air space” within their unit in a multi-unit development. This means that the condo owner’s title to the property does not include the four walls that divide their unit from other units or common areas in the property. The floor, ceiling, sidewalks, stairwells, and exterior areas are all part of the common ownership of the condo—known as limited common elements.

One common type of condominium is a residential high-rise that provides housing for several different families. However, the concept is not limited to high-rise buildings or residential properties. Residential townhouses are sometimes developed as condominiums. Commercial properties, like office buildings, can also be structured as condos.

Important

Condos, like apartments, suit those who prefer shared community living without the hassle of maintenance tasks such as lawn care and property management.

Key Considerations for Condominium Buyers

Developers offer parking spaces and garages to unit owners in different ways. In some developments, these spaces are reserved as limited common areas, and the condo association maintains ownership but gives exclusive rights for the unit owner to use the space or garage.

In other developments, the unit owner buys the garage or parking space and has ownership. However, the covenants, conditions, and restrictions may still limit the owner’s ability to sell or rent the space independent of the unit itself.

Comparing Condominiums and Apartments

The big difference between a condo and an apartment is that you generally own a condo, while you rent an apartment. Apartment buildings are usually owned by a single owner (such as a property management company), and the buildings are used solely for rental purposes. However, condos that are rented out to tenants are sometimes referred to as apartments.1

Thus, the only notable difference between a condominium and an apartment is ownership. A condo is generally something you own, while an apartment is something you rent.

Essential Condominium Ownership Requirements

The declaration of covenants, conditions, and restrictions is a legal document outlining rules for condo unit owners.

This document defines the acceptable use of the unit. It describes the owner’s use of limited common areas and general common areas. The declaration includes rules for selecting the board for the homeowners association. This board manages the development, directs repairs and maintenance of the common areas, and assesses fees.

Unit owners pay condo fees for insurance, shared utilities, and future maintenance reserves.

Condos may also include the fees the association pays to a management company for the daily operation of the development. Condo fees can rise, and major maintenance costs not covered by reserve funds may be charged to owners.

Weighing the Pros and Cons of Condo Living

Buying a home is usually a major investment, so it’s vital to know the pros and cons, especially for condos, due to financial, legal, and tax implications.

Pros

Shared amenities

Security services

Common area maintenance

Cons

Fees and special assessments

Less privacy

Additional restrictions from condo associations

Pros Explained

Shared amenities: Condo living affords its owners several benefits, such as access to amenities that are ordinarily only accessible at a cost. Owners can enjoy the exclusive use of swimming pools, tennis courts, and fitness facilities at no extra cost. Some high-end condos even provide access to spas, rooftop entertainment spaces, and gardens.

Security services: Many condo associations employ security services to safeguard their community and protect their residents. This may be as simple as a gate and a doorman in the front lobby. It can also be more complex, such as camera surveillance or patrols by security personnel. Either way, the community benefits from extra eyes warding off would-be intruders and additional peace of mind as a result.

Common area maintenance: Condo associations are responsible for maintaining common areas such as the amenities. Owners can enjoy the facilities without worrying about cleaning them.

Cons Explained

Fees and special assessments: Condo owners must pay association fees for community upkeep, covering common areas, exteriors, and some interior maintenance. Fees can vary according to what they support. For major repairs, condo owners may be assessed a special fee to cover the costs. These special assessments can be thousands or tens of thousands of dollars.

Less privacy: Much like apartments, condos often share common walls, as well as common spaces. Living in proximity and sharing walls and spaces limits the amount of privacy one can enjoy. In contrast to single-family detached houses, residents must tolerate neighborly nuisances.

Additional restrictions from condo associations: Condos are managed by condo associations that impose certain rules and restrictions on owners. The condo association governs how common spaces can be used, to what extent condo owners can make improvements or changes to their units, and sometimes who can enjoy those spaces with them.

What Does Condo Mean?

A condo, short for condominium, is an individually owned residential unit in a building or complex composed of other residential units. Condo owners share a common space and often pay association fees to maintain the common space, amenities, and other shared resources.

What Is the Difference Between an Apartment and a Condo?

Apartments are individual residential units within a building or complex that are rented by their occupants. The entire building is usually owned by a property management company. In contrast, condos are residential units within a building or complex that are separately owned.

Are Condos Cheaper Than Houses?

Condos are generally less expensive than single-family houses in the same area. Condo owners pay an association fee that covers maintenance costs, amenities, and other resources. These fees are generally less than the costs to maintain a house. However, some condos, especially luxury condos in affluent areas, can command much more than the average house.

Are Condos Cheaper Than Apartments?

The direct cost to reside in the unit can be more expensive than owning a condo since the owner will charge more than the cost of a mortgage to make a profit. However, on average, renting an apartment is less expensive than owning a condo, as apartment renters do not pay association fees. Condo owners must also pay for maintenance and repairs, while apartment renters do not.

What Is a Condo Assessment?

An assessment is a fee billed to condo owners for major repairs or enhancements not covered by the regular condo fees. The assessment fee is generally based on the size of the unit. If all units are the same size, each owner will pay an equal assessment amount.

The Bottom Line

Condominiums are individually owned residential units within a larger complex. Condo owners own their units but share common areas, amenities, and other resources.

Monthly condominium fees are necessary for amenities, maintenance, upkeep of community property, and possible special assessments for major repairs. While condos have these added fees, they are generally less expensive than single-family houses.

Pros of condo living include shared amenities and security, while cons include less privacy and restrictions from condo associations.

It’s important to understand the declaration of covenants, conditions, and restrictions involved in condominium ownership. Consider all the implications and carefully weigh the pros and cons before deciding whether to buy a condo.

Sponsored

Take a Position

Interactive Brokers offers access to exchange-listed Forecast and Event Contracts on ForecastTrader. In addition to trading stocks and ETFs, traders can seamlessly trade on yes-or-no contracts across categories like elections, sports, climate, and more. Plus, real-time pricing and data, extended trading hours, and incentive coupons for eligible account users. Enjoy $0 commissions and low execution fees. Open a ForecastTrader account today.

The New Civil Code of the Philippinesdefines a contract of sale as a contract whereby one of the contracting parties obligates himself to transfer the ownership of and to deliver a determinate thing, and the other to pay therefor a price certain in money or its equivalent. In view of the said definition, Contract of Sale, by its very nature, is a consensual contract because it is perfected by mere consent. The essential elements of a contract of sale are the following:

Consent or meeting of the minds, that is, consent to transfer ownership in exchange for the price;

Determinate subject matter; and

Price certain in money or its equivalent.

Under this definition, a contract to sell may not be considered as a contract of salebecause the first essential element is lacking. In a contract to sell, the prospective seller explicitly reserves the transfer of title to the prospective buyer, meaning, the prospective seller does not as yet agree or consent to transfer ownership of the property subject of the contract to sell until the happening of an event, which for present purposes we shall take as the full payment of the purchase price. What the seller agrees or obliges himself to do is to fulfill his promise to sell the subject property when the entire amount of the purchase price is delivered to him. In other words, the full payment of the purchase price partakes of a suspensive condition, the non-fulfillment of which prevents the obligation to sell from arising and thus, ownership is retained by the prospective seller without further remedies by the prospective buyer (Coronel vs. Court of Appeals 263 SCRA 15, October 07, 1996).

In Roque vs. Lapuz (96 SCRA 741 [1980]), the Supreme Court had occasion to rule that the contract between the parties was a contract to sell where the ownership or title is retained by the seller and is not to pass until the full payment of the price, such payment being a positive suspensive condition and failure of which is not a breach, casual or serious, but simply an event that prevented the obligation of the vendor to convey title from acquiring binding force. Stated positively, upon the fulfillment of the suspensive condition which is the full payment of the purchase price, the prospective seller’s obligation to sell the subject property by entering into a contract of sale with the prospective buyer becomes demandable as provided in Article 1479 of the Civil Code which states:

Art. 1479. A promise to buy and sell a determinate thing for a price certain is reciprocally demandable.

An accepted unilateral promise to buy or to sell a determinate thing for a price certain is binding upon the promisor if the promise is supported by a consideration distinct from the price.

Thus, a contract to sell may be defined as a bilateral contract whereby the prospective seller, while expressly reserving the ownership of the subject property despite delivery thereof to the prospective buyer, binds himself to sell the said property exclusively to the prospective buyer upon fulfillment of the condition agreed upon, that is, full payment of the purchase price.

A contract to sell as defined hereinabove, may not even be considered as a conditional contract of sale where the seller may likewise reserve title to the property subject of the sale until the fulfillment of a suspensive condition, because in a conditional contract of sale, the first element of consent is present, although it is conditioned upon the happening of a contingent event which may or may not occur. If the suspensive condition is not fulfilled, the perfection of the contract of sale is completely abated (Homesite and housing Corp. vs. Court of Appeals, 133 SCRA 777 [1984]). However, if the suspensive condition is fulfilled, the contract of sale is thereby perfected, such that if there had already been previous delivery of the property subject of the sale to the buyer, ownership thereto automatically transfers to the buyer by operation of law without any further act having to be performed by the seller.

In a contract to sell, upon the fulfillment of the suspensive condition which is the full payment of the purchase price, ownership will not automatically transfer to the buyer although the property may have been previously delivered to him. The prospective seller still has to convey title to the prospective buyer by entering into a contract of absolute sale.

Importance of Knowing the Difference between Contract to Sell and Contract of Sale

It is essential to distinguish between a contract to sell and a conditional contract of sale specially in cases where the subject property is sold by the owner not to the party the seller contracted with, but to a third person, as in the case at bench. In a contract to sell, there being no previous sale of the property, a third person buying such property despite the fulfillment of the suspensive condition such as the full payment of the purchase price, for instance, cannot be deemed a buyer in bad faith and the prospective buyer cannot seek the relief of reconveyance of the property. There is no double sale in such case. Title to the property will transfer to the buyer after registration because there is no defect in the owner-seller’s title per se, but the latter, of course, may be used for damages by the intending buyer (Coronel vs. Court of Appeals).

In a conditional contract of sale, however, upon the fulfillment of the suspensive condition, the sale becomes absolute and this will definitely affect the seller’s title thereto. In fact, if there had been previous delivery of the subject property, the seller’s ownership or title to the property is automatically transferred to the buyer such that, the seller will no longer have any title to transfer to any third person. Applying Article 1544 of the Civil Code, such second buyer of the property who may have had actual or constructive knowledge of such defect in the seller’s title, or at least was charged with the obligation to discover such defect, cannot be a registrant in good faith. Such second buyer cannot defeat the first buyer’s title. In case a title is issued to the second buyer, the first buyer may seek reconveyance of the property subject of the sale (Ibid).

With the above postulates as guidelines, contracting parties may now proceed to the task of deciphering the real nature of the contract they entered into.

What Is Commercial Real Estate (CRE)?

Commercial real estate (CRE) encompasses properties used for business activities rather than residential purposes. It includes a diverse range of properties, from single retail stores to expansive industrial complexes, often leased to tenants for income through rent or business operations. Leasing terms in CRE can significantly differ from residential agreements, offering unique investment opportunities and challenges.

The business of commercial real estate involves the construction, marketing, management, and leasing of property for business use.

There are many categories of commercial real estate such as retail and office space, hotels and resorts, strip malls, restaurants, and healthcare facilities.

Distinguishing Commercial From Residential Real Estate

Real estate is mainly categorized as commercial or residential.

Residential properties are structures reserved for human habitation rather than commercial or industrial use. As its name implies, commercial real estate is used in commerce, and multiunit rental properties that serve as residences for tenants are classified as commercial activity for the landlord.

Commercial real estate is typically categorized into four classes, depending on function:

Individual categories may also be further classified. There are, for instance, different types of retail real estate:

Hotels and resorts

Strip malls

Restaurants

Healthcare facilities

Similarly, office space has several subtypes. Office structures are often characterized as class A, class B, or class C:

Class A represents the best buildings in terms of aesthetics, age, quality of infrastructure, and location.

Class B buildings are older and not as competitive—price-wise—as class A buildings. Investors often target these buildings for restoration.

Class C buildings are the oldest, usually more than 20 years of age, and may be located in less attractive areas and in need of maintenance.

Some zoning and licensing authorities further break out industrial properties, which are sites used for the manufacture and production of goods, especially heavy goods. Most consider industrial properties to be a subset of commercial real estate.

Navigating Commercial Lease Agreements

Some businesses own the buildings that they occupy. More commonly, commercial property is leased. An investor or a group of investors owns the building and collects rent from each business that operates there.

Commercial lease rates—the price to occupy a space over a stated period—are customarily quoted in annual rental dollars per square foot. (Residential real estate rates are quoted as an annual sum or a monthly rent.)

Commercial leases typically run from one year to 10 years or more, with office and retail space typically averaging five- to 10-year leases. This, too, is different from residential real estate, where yearly or month-to-month leases are common.

The Roles of a Property Manager: Keeping Real Estate Investments Profitable and Well-Maintained

Real estate ownership can be a rewarding investment, but managing properties effectively requires time, expertise, and attention to detail. This is where property managers play a crucial role. Whether handling residential, commercial, or mixed-use developments, property managers ensure that properties operate efficiently, tenants remain satisfied, and owners achieve their investment goals.

What is a Property Manager?

A property manager is a professional responsible for overseeing the daily operations, maintenance, and administration of a property on behalf of the owner. They act as the bridge between property owners and tenants, ensuring that the property remains profitable, compliant, and well-maintained.

Property managers are commonly employed for condominiums, apartment buildings, office spaces, retail centers, and residential subdivisions.

Key Roles and Responsibilities of a Property Manager

1. Tenant Management

One of the primary responsibilities of a property manager is handling tenant-related concerns. This includes:

Marketing vacant units

Screening prospective tenants

Processing lease agreements

Handling tenant inquiries and complaints

Managing lease renewals and terminations

Effective tenant management helps maintain high occupancy rates and positive tenant relationships.

2. Property Maintenance and Repairs

Property managers ensure that buildings, facilities, and common areas remain in excellent condition. Their responsibilities include:

Conducting regular property inspections

Coordinating preventive maintenance programs

Scheduling repairs and renovations

Supervising contractors and service providers

Ensuring safety and cleanliness standards

Well-maintained properties retain their value and attract quality tenants.

3. Financial Management

Property managers are responsible for overseeing the financial performance of a property. Key tasks include:

Collecting rent and association dues

Monitoring operating expenses

Preparing budgets and financial reports

Managing vendor payments

Recommending strategies to improve profitability

Proper financial management helps maximize returns for property owners.

4. Lease Administration

Managing lease agreements is a critical part of property management. Property managers:

Prepare and review lease contracts

Ensure compliance with lease terms

Monitor rental escalations

Handle renewals and amendments

Address lease violations when necessary

Effective lease administration protects both owners and tenants.

5. Legal and Regulatory Compliance

Property managers help ensure compliance with applicable laws, regulations, and local ordinances. This includes:

Building and safety regulations

Fire safety requirements

Environmental standards

Local government permits

Property tax and documentation requirements

Compliance reduces legal risks and protects the property’s reputation.

6. Risk Management and Security

Property managers identify potential risks and implement measures to protect the property and its occupants. Their responsibilities may include:

Monitoring security systems

Coordinating emergency response procedures

Managing insurance requirements

Conducting safety inspections

Addressing potential hazards

A proactive approach to risk management helps prevent costly incidents.

7. Vendor and Contractor Coordination

Property managers work with various service providers, including:

Maintenance personnel

Security agencies

Landscaping contractors

Cleaning services

Utility providers

They ensure that services are delivered efficiently and within budget.

Benefits of Hiring a Property Manager

Improved Property Performance

Professional management helps maintain property value and operational efficiency.

Higher Tenant Satisfaction

Prompt responses to tenant concerns lead to better tenant retention and occupancy rates.

Time Savings for Owners

Property owners can focus on investment growth while managers handle day-to-day operations.

Better Financial Control

Property managers monitor expenses, collect payments, and provide accurate financial reporting.

Legal Protection

Experienced property managers help ensure compliance with laws and regulations, reducing potential liabilities.

Skills of an Effective Property Manager

Successful property managers typically possess:

Strong communication skills

Leadership and organizational abilities

Financial management expertise

Problem-solving capabilities

Knowledge of real estate laws and regulations

Customer service orientation

These skills allow them to effectively manage properties while balancing the needs of owners and tenants.

Appraisal of Real Property: Understanding the True Value of Real Estate

Real property appraisal is the process of determining the market value of a property at a specific point in time. It is an essential part of the real estate industry, helping buyers, sellers, investors, banks, and government agencies make informed decisions regarding property transactions.

Whether you are purchasing a home, selling a condominium, investing in commercial real estate, or applying for a mortgage, a professional appraisal provides an objective and unbiased estimate of a property’s value.

What is Real Property Appraisal?

Real property appraisal is the systematic evaluation of land and any improvements attached to it, such as buildings, houses, and other structures. The goal is to estimate the property’s fair market value based on various factors, including location, size, condition, and current market trends.

Licensed real estate appraisers use recognized valuation methods and industry standards to arrive at an accurate valuation.

Why is Property Appraisal Important?

1. Supports Property Sales and Purchases

An appraisal helps buyers and sellers determine a fair price for a property. It minimizes the risk of overpricing or undervaluing real estate assets.

2. Assists in Mortgage Lending

Banks and financial institutions require appraisals before approving loans. This ensures that the property’s value is sufficient to secure the loan amount.

3. Guides Investment Decisions

Real estate investors rely on appraisals to assess profitability and potential returns before purchasing properties.

4. Establishes Tax Assessments

Local government units use property valuations as a basis for real property taxation and assessment purposes.

5. Supports Legal Proceedings

Property appraisals are often needed in cases involving estate settlements, expropriation, partition of property, divorce, and other legal matters.

Factors Affecting Property Value

Several factors influence the value of a property, including:

Location and accessibility

Lot size and shape

Building size and condition

Neighborhood development

Availability of utilities and amenities

Economic conditions

Market demand and supply

Zoning and land-use regulations

Properties located near business districts, schools, hospitals, transportation hubs, and commercial centers generally command higher values.

Common Methods of Real Property Appraisal

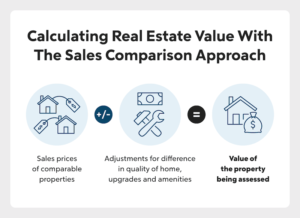

1. Sales Comparison Approach

This method compares the subject property with similar properties that have recently been sold in the same area. Adjustments are made for differences in size, location, age, and features.

This is the most commonly used approach for residential properties.

2. Cost Approach

The cost approach estimates the value of a property by calculating the cost to replace or reproduce the improvements, less depreciation, plus the value of the land.

This method is commonly used for new buildings and special-purpose properties.

3. Income Capitalization Approach

This approach determines value based on the income-generating potential of a property. It is widely used for commercial buildings, rental properties, and investment real estate.

The higher the expected income, the greater the property’s value.

The Real Property Appraisal Process

A typical appraisal process includes:

Property inspection

Collection of market data

Analysis of comparable sales

Evaluation of physical and legal characteristics

Application of valuation approaches

Preparation of the appraisal report

Final opinion of value

The final appraisal report contains detailed findings, supporting data, valuation calculations, and the appraiser’s professional opinion of value.

Challenges in Property Appraisal

Real estate markets are constantly changing due to economic conditions, infrastructure developments, and shifts in buyer preferences. Appraisers must stay updated with market trends and maintain professional judgment to provide accurate and reliable valuations.

Factors such as limited comparable sales, unique property characteristics, and rapidly changing market conditions can also affect the appraisal process.

Conclusion

Real property appraisal plays a crucial role in the real estate industry by providing an objective estimate of a property’s value. It serves as a foundation for buying, selling, financing, investing, taxation, and legal transactions. Through proper valuation methods and professional expertise, appraisers help ensure transparency, fairness, and confidence in the real estate market.

Understanding the importance of property appraisal enables property owners, investors, and stakeholders to make informed decisions and maximize the value of their real estate assets.

Assessment of Real property

Assessment of Real Property: A Key Component of Property Taxation

Real property assessment is the process of determining the taxable value of land, buildings, and other improvements for taxation purposes. It is an important function of local government units (LGUs) as it serves as the basis for computing real property taxes that help fund public services and infrastructure projects.

Property assessment differs from property appraisal. While appraisal focuses on determining the market value of a property, assessment focuses on establishing its assessed value for taxation purposes.

What is Real Property Assessment?

Real property assessment is the official valuation of real estate conducted by government assessors to determine the amount of property tax that a property owner must pay. The assessment process considers the property’s market value and applies an assessment level prescribed by law.

The resulting assessed value becomes the basis for calculating real property taxes.

Importance of Real Property Assessment

1. Generates Government Revenue

Real property taxes collected through assessments provide funding for public schools, roads, healthcare facilities, and other community services.

2. Promotes Fair Taxation

A proper assessment ensures that property owners pay taxes based on the value of their properties, creating a fair and equitable tax system.

3. Supports Urban Development

Accurate property assessments help local governments plan and implement development projects effectively.

4. Maintains Updated Property Records

The assessment process helps keep property ownership, land use, and valuation records current and organized.

Factors Considered in Property Assessment

Assessors evaluate various factors when determining a property’s value, including:

Location of the property

Land area and dimensions

Building size and improvements

Property classification

Current market conditions

Accessibility and infrastructure

Actual use of the property

Properties located in prime commercial areas generally receive higher assessments than those in less developed locations.

Property Classifications

Real properties are commonly classified into the following categories:

Residential

Properties used primarily for housing purposes, such as houses, condominiums, and residential lots.

Commercial

Properties used for business activities, including offices, retail establishments, and shopping centers.

Industrial

Properties utilized for manufacturing, warehousing, and industrial operations.

Agricultural

Land used for farming, livestock production, and agricultural activities.

Special Purpose

Properties used for schools, hospitals, religious institutions, and government facilities.

The Real Property Assessment Process

The assessment process typically involves:

Property identification and classification

Determination of market value

Application of assessment levels

Computation of assessed value

Recording and updating assessment records

Issuance of tax declarations

Local assessors regularly review property records to ensure that assessments remain accurate and consistent with market conditions.

Challenges in Real Property Assessment

Assessors often face challenges such as rapidly changing property values, incomplete records, unauthorized improvements, and varying market conditions. Maintaining updated data and conducting regular reassessments are essential to ensuring fair taxation.

Conclusion

Real property assessment is a vital process that supports local government operations and public services through the collection of real property taxes. By determining the taxable value of properties accurately and fairly, assessment promotes transparency, equity, and efficient governance. Understanding how property assessment works helps property owners appreciate their tax responsibilities and the role these taxes play in community development.

make me a blog content for my website

Assessment of Real Property: Why It Matters to Every Property Owner

Owning real estate comes with many benefits, but it also comes with responsibilities. One of the most important aspects of property ownership is understanding real property assessment. Whether you own a residential lot, condominium unit, commercial building, or agricultural land, property assessment plays a significant role in determining your tax obligations and the overall value of your investment.

What is Real Property Assessment?

Real property assessment is the process of determining the value of a property for taxation purposes. Conducted by local government assessors, the assessment establishes the property’s assessed value, which serves as the basis for calculating real property taxes.

Unlike an appraisal, which estimates a property’s market value for buying, selling, or financing purposes, assessment focuses on taxation and government revenue generation.

Why Property Assessment is Important

Fair Property Taxation

A properly assessed property ensures that owners pay taxes based on the property’s actual value. This creates a fair taxation system where property owners contribute equitably to local government funding.

Supports Community Development

Real property taxes collected through assessments help finance essential public services, including:

Road construction and maintenance

Public schools

Healthcare facilities

Parks and recreational areas

Disaster preparedness programs

By paying property taxes, owners directly contribute to the growth and development of their communities.

Protects Property Records

The assessment process helps maintain updated records regarding ownership, land use, improvements, and property classifications. Accurate records are essential for legal transactions and future property development.

Factors That Affect Property Assessment

Several factors influence the assessed value of a property, including:

Location

Properties located near business districts, schools, hospitals, transportation hubs, and major infrastructure projects generally have higher assessed values.

Property Size

The total land area and building floor area significantly impact the property’s valuation.

Property Classification

Residential, commercial, industrial, and agricultural properties have different assessment levels depending on their use.

Improvements and Developments

Additional structures, renovations, and property enhancements can increase assessed value.

Market Conditions

Changes in real estate demand, economic growth, and infrastructure development may affect property values over time.

The Property Assessment Process

The assessment process typically includes:

Property Inspection

Assessors gather information about the property’s physical characteristics and current use.

Property Classification

The property is categorized based on its primary use, such as residential, commercial, industrial, or agricultural.

Valuation

The market value of the property is determined using available data and valuation standards.

Application of Assessment Levels

An assessment level is applied to the market value to determine the assessed value.

Tax Computation

The assessed value serves as the basis for calculating the real property tax due.

Common Property Assessment Challenges

Property owners sometimes encounter issues such as:

Outdated property records

Incorrect property classifications

Unreported improvements

Disputes regarding assessed values

Regularly reviewing property records and tax declarations can help prevent these issues and ensure accurate assessments.

Tips for Property Owners

To ensure a smooth assessment process, property owners should:

Keep ownership documents updated.

Report any major property improvements.

Verify information in tax declarations.

Monitor changes in local property assessments.

Consult qualified real estate professionals when necessary.

Appraisal of Real Property: Understanding the True Value of Real Estate

Real property appraisal is the process of determining the market value of a property at a specific point in time. It is an essential part of the real estate industry, helping buyers, sellers, investors, banks, and government agencies make informed decisions regarding property transactions.

Whether you are purchasing a home, selling a condominium, investing in commercial real estate, or applying for a mortgage, a professional appraisal provides an objective and unbiased estimate of a property’s value.

What is Real Property Appraisal?

Real property appraisal is the systematic evaluation of land and any improvements attached to it, such as buildings, houses, and other structures. The goal is to estimate the property’s fair market value based on various factors, including location, size, condition, and current market trends.

Licensed real estate appraisers use recognized valuation methods and industry standards to arrive at an accurate valuation.

Why is Property Appraisal Important?

1. Supports Property Sales and Purchases

An appraisal helps buyers and sellers determine a fair price for a property. It minimizes the risk of overpricing or undervaluing real estate assets.

2. Assists in Mortgage Lending

Banks and financial institutions require appraisals before approving loans. This ensures that the property’s value is sufficient to secure the loan amount.

3. Guides Investment Decisions

Real estate investors rely on appraisals to assess profitability and potential returns before purchasing properties.

4. Establishes Tax Assessments

Local government units use property valuations as a basis for real property taxation and assessment purposes.

5. Supports Legal Proceedings

Property appraisals are often needed in cases involving estate settlements, expropriation, partition of property, divorce, and other legal matters.

Factors Affecting Property Value

Several factors influence the value of a property, including:

Location and accessibility

Lot size and shape

Building size and condition

Neighborhood development

Availability of utilities and amenities

Economic conditions

Market demand and supply

Zoning and land-use regulations

Properties located near business districts, schools, hospitals, transportation hubs, and commercial centers generally command higher values.

Common Methods of Real Property Appraisal

1. Sales Comparison Approach

This method compares the subject property with similar properties that have recently been sold in the same area. Adjustments are made for differences in size, location, age, and features.

This is the most commonly used approach for residential properties.

2. Cost Approach

The cost approach estimates the value of a property by calculating the cost to replace or reproduce the improvements, less depreciation, plus the value of the land.

This method is commonly used for new buildings and special-purpose properties.

3. Income Capitalization Approach

This approach determines value based on the income-generating potential of a property. It is widely used for commercial buildings, rental properties, and investment real estate.

The higher the expected income, the greater the property’s value.

The Real Property Appraisal Process

A typical appraisal process includes:

Property inspection

Collection of market data

Analysis of comparable sales

Evaluation of physical and legal characteristics

Application of valuation approaches

Preparation of the appraisal report

Final opinion of value

The final appraisal report contains detailed findings, supporting data, valuation calculations, and the appraiser’s professional opinion of value.

Challenges in Property Appraisal

Real estate markets are constantly changing due to economic conditions, infrastructure developments, and shifts in buyer preferences. Appraisers must stay updated with market trends and maintain professional judgment to provide accurate and reliable valuations.

Factors such as limited comparable sales, unique property characteristics, and rapidly changing market conditions can also affect the appraisal process.

The Land Development Method in Real Estate

The Land Development Method is an important valuation approach used in real estate to estimate the value of undeveloped land or land with strong development potential. This method is commonly applied when land is intended for future projects such as residential subdivisions, commercial centers, industrial parks, condominiums, or mixed-use developments. It helps developers, investors, and appraisers determine whether a project is financially feasible and if the land can generate profitable returns.

In simple terms, the land development method calculates the value of land by analyzing what the completed project may be worth in the future. From the projected selling price or total revenue of the finished development, all estimated costs are deducted. These costs may include construction expenses, permits, legal fees, infrastructure, labor, utilities, financing charges, marketing costs, and the developer’s expected profit. The remaining amount represents the estimated present value of the land.

This valuation method is especially useful for raw or vacant land that does not yet produce income. Since undeveloped land may not have immediate market value based on rental income or existing structures, the land development method focuses on its future potential. This makes it a practical tool for project feasibility studies and long-term investment analysis.

One major advantage of the land development method is that it helps developers evaluate whether a proposed project is worth pursuing. It provides a clear estimate of expected profitability, assists in budgeting, and supports strategic planning. Investors can also use this method to compare risks and returns before committing capital to development projects.

However, the accuracy of this method depends on realistic assumptions. If projected selling prices, construction costs, market demand, or timelines are inaccurate, the valuation may also be affected. Because of this, careful market research, cost estimation, and financial planning are essential.

In conclusion, the Land Development Method plays a vital role in real estate valuation and development planning. By estimating land value based on future development potential and deducting all related expenses, this method helps developers, investors, and appraisers make informed and profitable decisions. It remains one of the most effective tools for evaluating raw land and planning successful real estate projects.

Valuation Methodology in Real Estate

Valuation methodology is one of the most important concepts in real estate because it helps determine the true value of a property. Whether for buying, selling, financing, taxation, or investment purposes, accurate property valuation is essential for making informed decisions. In simple terms, valuation methodology refers to the systematic process used by appraisers, investors, and real estate professionals to estimate the market value of land, buildings, or other real estate assets.

There are different valuation methodologies used depending on the type of property and its purpose. One of the most common is the Sales Comparison Approach. This method determines property value by comparing it to similar properties that have recently been sold in the same location. Adjustments are made based on factors such as size, design, condition, and amenities. This approach is commonly used for residential properties because it reflects actual market behavior.

Another widely used method is the Cost Approach. This method estimates the value of a property by calculating how much it would cost to rebuild or replace the structure, then subtracting depreciation, and adding the land value. The cost approach is often used for newly built properties, schools, hospitals, and special-purpose buildings where comparable sales may be limited.

The Income Capitalization Approach is another important valuation method, mainly used for commercial and income-generating properties such as apartments, office buildings, malls, and hotels. This approach determines value based on the income a property can produce. Investors often rely on this method to evaluate profitability and long-term return on investment.

Another useful method is the Residual Method, commonly applied in land development and project feasibility analysis. It estimates land value by deducting construction costs, development expenses, and expected profit from the projected selling price of the completed project.

Valuation methodology plays a major role in real estate because it provides a reliable basis for fair pricing and sound decision-making. It helps buyers avoid overpaying, supports sellers in pricing properties competitively, assists banks in mortgage and loan approvals, and guides investors in analyzing profitable opportunities.

In conclusion, valuation methodology is a foundation of real estate appraisal and investment. By using methods such as sales comparison, cost approach, income capitalization, and residual analysis, professionals can determine accurate and realistic property values. Understanding these methods is essential for anyone involved in real estate, whether as a buyer, seller, developer, appraiser, or investor.